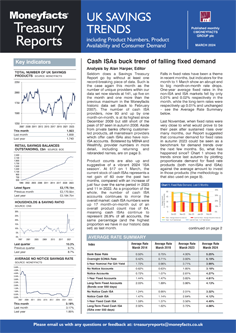

Rachel Springall, Finance Expert at Moneyfacts, said:

“Cash ISAs stole the show in March, with providers working hard to entice savers in the run-up to end of the tax-year. The number of Cash ISAs rose to its highest level in almost six months, and average rates across easy access, notice and one-year fixed Cash ISAs rose. Those savers looking for some flexibility with their cash may be pleased to see the average easy access ISA rate stands at its highest point in more than 15 years and the average notice ISA rate rose for the first time this year. Investors prepared to lock away their cash for the next 12 months may find it encouraging that the average one-year fixed ISA rate rose and broke its chain of five consecutive months of cuts.

“Outside of Cash ISAs, savers may be disappointed to see average rates across easy access, notice, one-year and longer-term bonds failed to rise between the start of March and the start of April. However, months of fixed rate cutting turmoil has dissipated, with rates seeing much more marginal cuts. The average one-year fixed bond rate fell by 0.01% month-on-month, the same percentage drop felt a month prior, which compares to a much more sizeable drop of 0.25% between January and February. The average shelf-life of a fixed rate bond rose to 36 days, from 27 days a month previously, indicating a more stable market. These movements will make it easier for providers and consumers to keep abreast of changes, but could also calm any knee-jerk rate cutting from providers who find themselves too far up the top rate tables and unable to cope with demand.

“Growing product choice is good news for savers, as more providers on the savings market can encourage competition. The number of savings account providers stands at a record high, with Plum entering the Cash ISA market and securing a position in the top rate tables to entice new customers. It may well be wise for savers to consider these more unfamiliar brands when comparing deals. Challenger banks can have lower administrative costs and are able to offer higher rates than other brands, but they can also change offers quickly, so speed is crucial to grab a top rate.”

Rachel Springall, Finance Expert at Moneyfacts, said:

“Cash ISAs stole the show in March, with providers working hard to entice savers in the run-up to end of the tax-year. The number of Cash ISAs rose to its highest level in almost six months, and average rates across easy access, notice and one-year fixed Cash ISAs rose. Those savers looking for some flexibility with their cash may be pleased to see the average easy access ISA rate stands at its highest point in more than 15 years and the average notice ISA rate rose for the first time this year. Investors prepared to lock away their cash for the next 12 months may find it encouraging that the average one-year fixed ISA rate rose and broke its chain of five consecutive months of cuts.

“Outside of Cash ISAs, savers may be disappointed to see average rates across easy access, notice, one-year and longer-term bonds failed to rise between the start of March and the start of April. However, months of fixed rate cutting turmoil has dissipated, with rates seeing much more marginal cuts. The average one-year fixed bond rate fell by 0.01% month-on-month, the same percentage drop felt a month prior, which compares to a much more sizeable drop of 0.25% between January and February. The average shelf-life of a fixed rate bond rose to 36 days, from 27 days a month previously, indicating a more stable market. These movements will make it easier for providers and consumers to keep abreast of changes, but could also calm any knee-jerk rate cutting from providers who find themselves too far up the top rate tables and unable to cope with demand.

“Growing product choice is good news for savers, as more providers on the savings market can encourage competition. The number of savings account providers stands at a record high, with Plum entering the Cash ISA market and securing a position in the top rate tables to entice new customers. It may well be wise for savers to consider these more unfamiliar brands when comparing deals. Challenger banks can have lower administrative costs and are able to offer higher rates than other brands, but they can also change offers quickly, so speed is crucial to grab a top rate.”