Rachel Springall, Finance Expert at Moneyfacts, said:

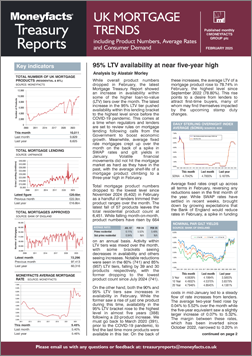

“Borrowers with a limited deposit may find it encouraging to see a growth in choice for mortgages available at 95% loan-to-value, now at its highest count in almost five years. There are now 388 options available, the highest level since March 2020, when there were 391 deals. This is positive to see, but there is still lots of room for more deals to be pushed out in this area of the market as it represents just 6% of all deals available to borrowers across fixed and variable mortgages. Despite rising choice, average rates across a two- or five-year fixed deal at 95% loan-to-value are higher than at the start of 2025. Overall product availability across the mortgage spectrum fell, but the average shelf-life of a deal rose month-on-month, which was largely expected due to the festive period when there are typically fewer changes from lenders.

“Lenders have been urged to do more to support first-time buyers, to boost growth in the economy, thus the debate on the loosening of lending rules. Therefore, there is an expectation for more products and innovation to emerge this year. However, the current rules will continue to pose a challenge for lenders to do more, as has been the case for the past 10 years where regulatory recommendations stipulate loan-to-income ratios of 4.5 or more do not exceed 15% of a lender’s new lending. Until lenders see a relaxation to these rules, some will have no choice but to pose limitations on those borrowing at higher loan-to-value tiers. Regardless of whether these rules change or not, there will be borrowers hoping to finish up their purchase before the stamp duty deadline at the end of March 2025.

“There has been a drop in swap rates over the past few weeks, but it can be a slow and steady process for lenders to move in the same direction. Borrowers may then be disheartened to know that fixed rates are not too dissimilar to what they were a year ago, with longer-term fixed rates somewhat higher. In truth, it can take a few weeks for lenders to catch up to a change in course on future rate expectations, or indeed to pass on reductions from any Bank of England base rate cuts, as the latter would be more immediately beneficial to borrowers sitting on a linked tracker rate. However, inflation is expected to rise in the coming months, which in turn makes it less likely for more base rate cuts. This will frustrate the millions of borrowers looking to remortgage in 2025 who plan to secure a fixed rate mortgage for peace of mind. After all, it remains the case that a fixed mortgage is much more affordable than falling onto a Standard Variable Rate (SVR), so borrowers about to come off a cheap deal must seek independent advice with urgency to assess the latest mortgages available to them.”

Rachel Springall, Finance Expert at Moneyfacts, said:

“Borrowers with a limited deposit may find it encouraging to see a growth in choice for mortgages available at 95% loan-to-value, now at its highest count in almost five years. There are now 388 options available, the highest level since March 2020, when there were 391 deals. This is positive to see, but there is still lots of room for more deals to be pushed out in this area of the market as it represents just 6% of all deals available to borrowers across fixed and variable mortgages. Despite rising choice, average rates across a two- or five-year fixed deal at 95% loan-to-value are higher than at the start of 2025. Overall product availability across the mortgage spectrum fell, but the average shelf-life of a deal rose month-on-month, which was largely expected due to the festive period when there are typically fewer changes from lenders.

“Lenders have been urged to do more to support first-time buyers, to boost growth in the economy, thus the debate on the loosening of lending rules. Therefore, there is an expectation for more products and innovation to emerge this year. However, the current rules will continue to pose a challenge for lenders to do more, as has been the case for the past 10 years where regulatory recommendations stipulate loan-to-income ratios of 4.5 or more do not exceed 15% of a lender’s new lending. Until lenders see a relaxation to these rules, some will have no choice but to pose limitations on those borrowing at higher loan-to-value tiers. Regardless of whether these rules change or not, there will be borrowers hoping to finish up their purchase before the stamp duty deadline at the end of March 2025.

“There has been a drop in swap rates over the past few weeks, but it can be a slow and steady process for lenders to move in the same direction. Borrowers may then be disheartened to know that fixed rates are not too dissimilar to what they were a year ago, with longer-term fixed rates somewhat higher. In truth, it can take a few weeks for lenders to catch up to a change in course on future rate expectations, or indeed to pass on reductions from any Bank of England base rate cuts, as the latter would be more immediately beneficial to borrowers sitting on a linked tracker rate. However, inflation is expected to rise in the coming months, which in turn makes it less likely for more base rate cuts. This will frustrate the millions of borrowers looking to remortgage in 2025 who plan to secure a fixed rate mortgage for peace of mind. After all, it remains the case that a fixed mortgage is much more affordable than falling onto a Standard Variable Rate (SVR), so borrowers about to come off a cheap deal must seek independent advice with urgency to assess the latest mortgages available to them.”